A rocky start to the year for stocks

The bumpiness so far could be a sign of things to come.

- The market has lost momentum and breadth as prospects for more rate cuts in 2025 have dimmed.

- Although I still believe we’re in a bull market (with earnings poised to potentially lift stocks higher), I believe we may be in the later stages, when things become more volatile.

- One particular source of volatility has been pressure from rising long-term interest rates, combined with high valuations.

- I believe rising long-term rates could be a recurring source of volatility for the market in 2025.

Recently, investors watched good news become bad news, as a stronger-than-expected jobs report sparked a market dip.

The market’s fears, of course, are that such a strong jobs picture gives the Fed even less leeway to cut interest rates further. Long-term interest rates ticked up that same day, with the yield on 10-year Treasurys climbing increasingly close to that 5% mark that has spooked stocks in recent past years.

While I continue to believe we are in a bull market—with rising earnings poised to pull the weight of the market still higher—this recent volatility could be a sign of things to come. Later stages of a bull market tend to be more volatile. And it doesn’t take as much to disrupt the market’s mojo when valuations like price-earnings (PE) ratios are high, as they have been. But moreover, I believe the interest-rate angst that’s been weighing on the market isn’t likely to go away anytime soon, and could be a recurring feature of the year ahead.

Here's a look at some of the trends that have caught my eye since the start of the year.

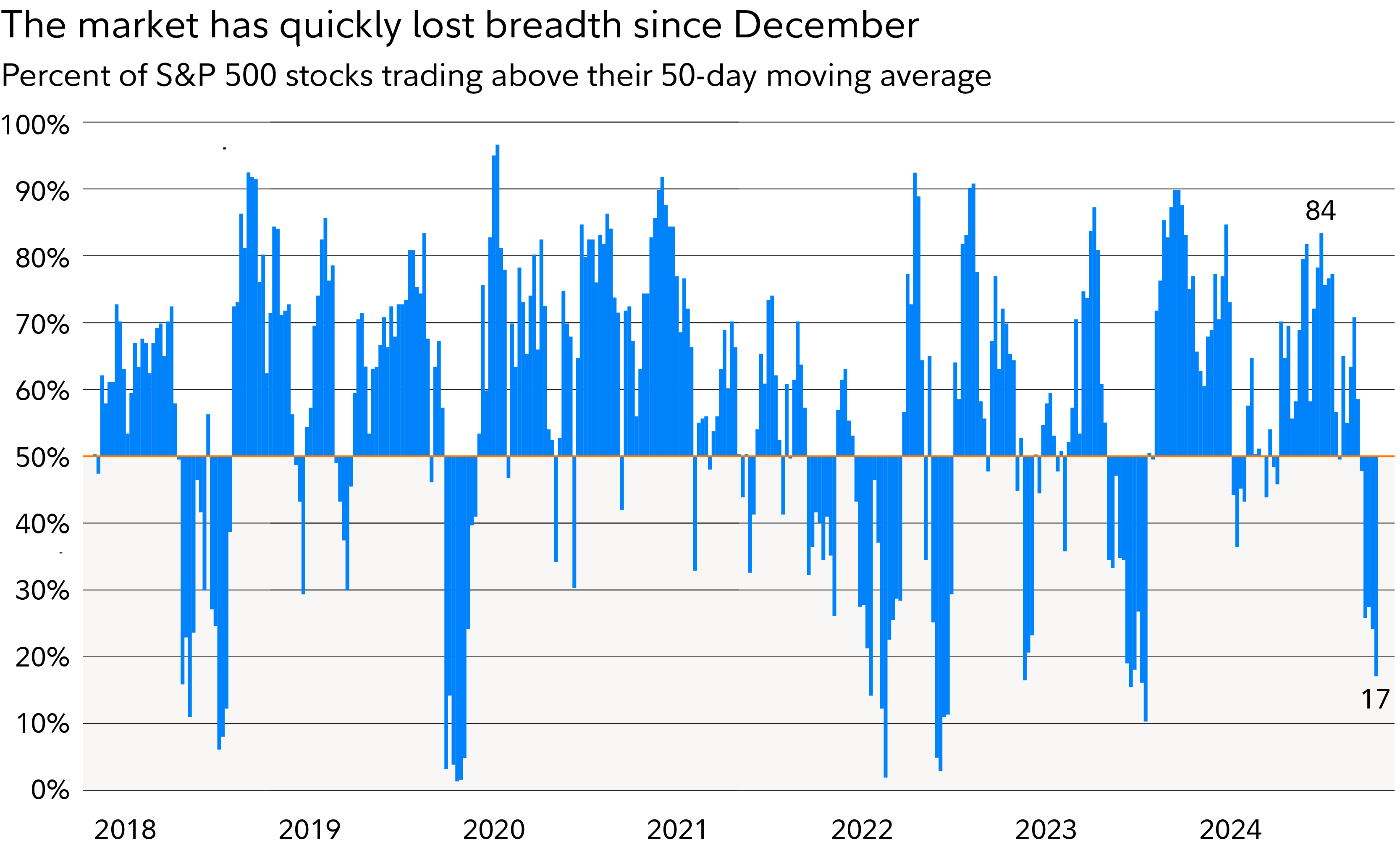

The broadening runs out of breadth

One of the big market stories in the second half of 2024 was the broadening, as market leadership seemed finally to pass from the “Magnificent 7” to the rest of the market, with a wide and varied range of stocks finally participating in and driving broad market gains.

Yet since mid-December (around when the Fed came out with reduced expectations for further rate cuts in 2025), the market has experienced a notable loss of momentum and breadth. As of last week, only 24% of stocks were trading above their 50-day moving average, and only 29% of S&P 500® stocks were outperforming the index. This was not what investors wanted to be seeing.

Past performance is no guarantee of future results. 50-day moving average calculated as average of stock's closing price over previous 50 days. Data as of January 13, 2025. Sources: FMRCo., Bloomberg, Haver Analytics.

One question this poses for investors is whether those narrow leadership trends could continue for yet another year. Given that trends in motion tend to stay in motion, the most likely answer might be “yes.” That said, these trends have been in motion for quite some time now—with large-cap growth stocks at the top of the 5-year-growth-rate leaderboard for the better part of the past decade.

At some point, mean reversion (the tendency for asset prices to return to their long-term trends over time) should kick in, and when it does it could be fierce. But when and from what level remains an elusive question. Timing tops and bottoms is always a low-success-rate undertaking, and in the case of the Magnificent 7 it has been especially so. To borrow a saying from the legendary former Fidelity fund manager Peter Lynch, selling your winners too soon can be “like cutting the flowers and watering the weeds.”

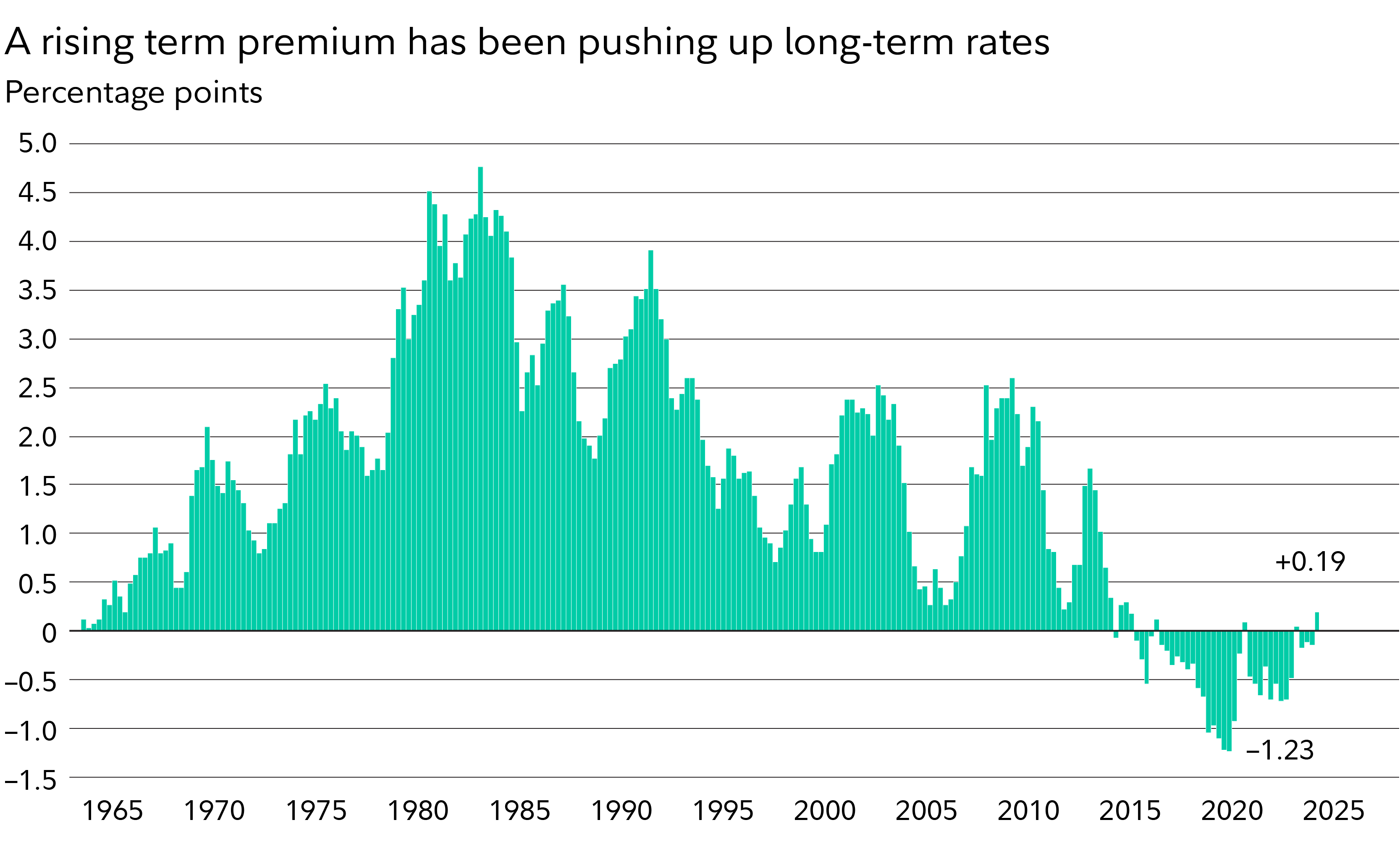

All about the rates

The recent market volatility experienced in mid-January, including the employment data, confirmed that the economy remains strong and the labor market remains tight.

At the same time, the yield curve has been steepening (meaning the difference between long-term rates and short-term rates has been widening), as 10-year Treasury yields have been rising.

This increase has seemed to be coming from a rise in the “term premium,” which refers to the additional compensation that lenders, like bondholders, typically require for lending for longer periods. After an unusual decade of negative term premiums—largely due to quantitative easing and zero or near-zero interest rates—it makes sense that this premium might start reverting to a more normal level, such as 1 to 1.5 percentage points.

Past performance is no guarantee of future results. Term premium is defined as the compensation that investors require for bearing the risk that interest rates may change over the life of a bond. Premium is calculated by the Federal Reserve Bank of New York using a 3-step linear regression model and a large number of pricing factors. Data as of January 13, 2025. Sources: FMRCo., Federal Reserve Bank of New York, Haver Analytics.

Why is the stock market now so sensitive to these changes? There are times when the stock market doesn’t pay too much attention to rates. But in periods of relatively high inflation, stocks and bonds tend to become positively correlated. One market model that has often worked in such periods is the “Fed model.” This theory holds that the interest rate on 10-year Treasurys and the earnings yield on stocks (meaning, earnings divided by price) should be roughly equivalent—or at least correlated—as investors pursue the highest yields.

Before the rate-induced bear market in 2022, 10-year Treasurys were 91% more expensive than stocks, according to this model, which left some cushion for stocks to do their own thing. But now, Treasurys are 15% cheaper than stocks on this measure, even though Treasurys are the lower-risk investment.

In short, given that valuation picture—plus the possibility that the term premium (and long yields along with it) might keep rising from here—I think this sensitivity to long interest rates could continue, and cause more stock-market angst in 2025.

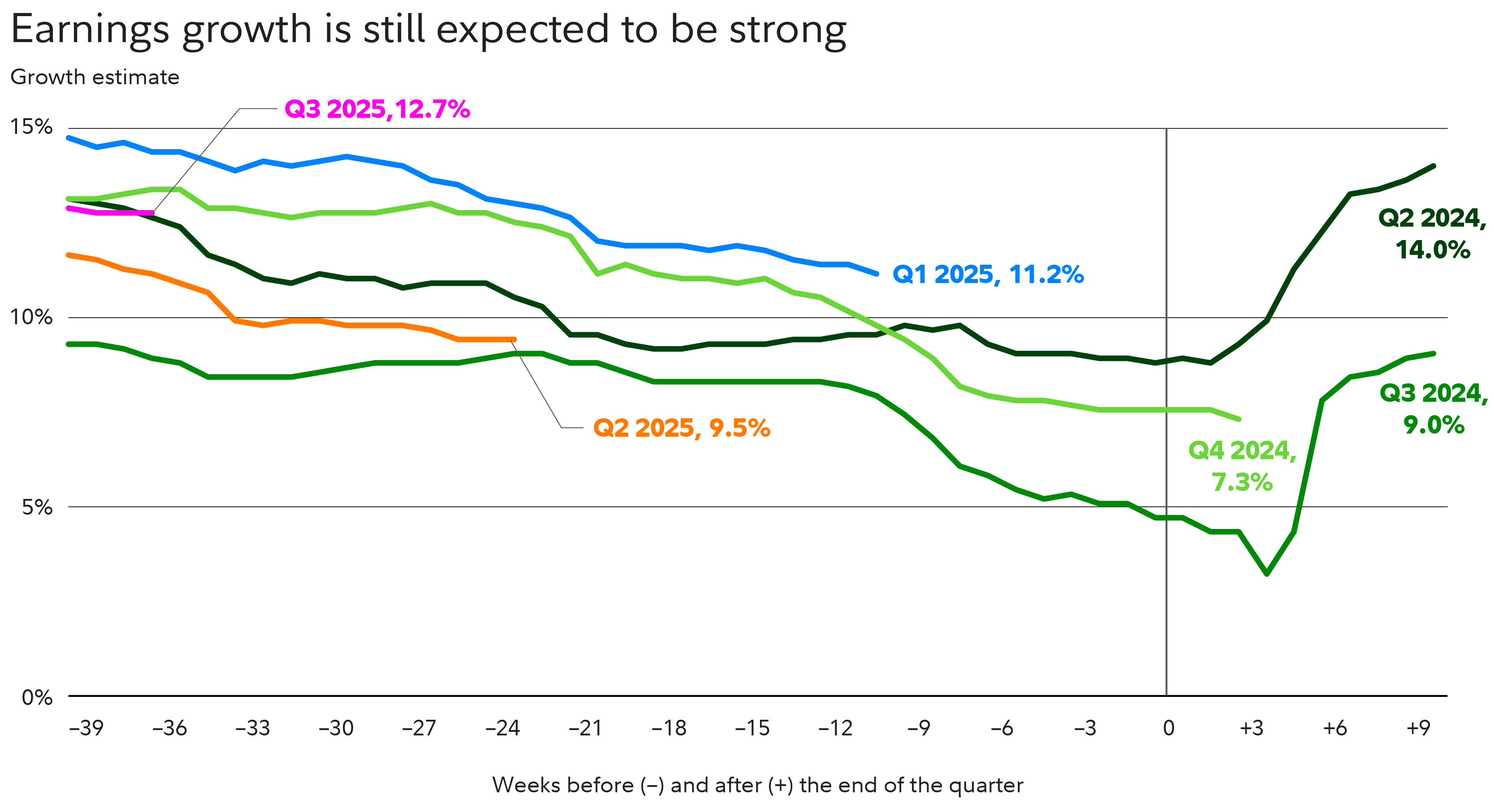

Watching for earnings growth to show up

All of that said, as I mentioned at the start, I believe rising earnings may help to soften some of these pressures, and could pull the market higher yet.

Fourth-quarter earnings season is just beginning, with consensus analyst expectations of 7% growth. If results follow a typical pattern of beating estimates, it could make for another double-digit quarter, which would help to dampen those valuation pressures.

Past performance is no guarantee of future results. Estimated earnings growth rate measured with consensus analyst estimates for S&P 500 companies. Data as of January 13, 2025. Source: Bloomberg.

While 2024 was a Goldilocks year of rising earnings and rising valuations, this year might see those forces pit against each other—with earnings growing but rising long-term rates pressuring valuations.

The main question for 2025 is where the opposing forces of growing earnings and rising rates may lead the market.

Next steps to consider

Asset Allocation

Leverage Fidelity’s extensive analytical, research, and management capabilities to level up your asset allocation approach.

Learn more

Sector/Industry

Target specific segments of the economy with our full spectrum of sector funds, ETFs, and other solutions.

Learn more

Quantitative Investing

Find out how a blend of human insight, data, and technology can help uncover opportunity for your clients.

Learn more

Views expressed are as of the date indicated, based on the information available at that time, and may change based on market or other conditions. Unless otherwise noted, the opinions provided are those of the speaker or author and not necessarily those of Fidelity Investments or its affiliates. Fidelity does not assume any duty to update any of the information.

Investing involves risk, including risk of loss.

Past performance and dividend rates are historical and do not guarantee future results.

Diversification and asset allocation do not ensure a profit or guarantee against loss.

Stock markets are volatile and can fluctuate significantly in response to company, industry, political, regulatory, market, or economic developments. Investing in stock involves risks, including the loss of principal.

In general, the bond market is volatile, and fixed income securities carry interest rate risk. (As interest rates rise, bond prices usually fall, and vice versa. This effect is usually more pronounced for longer-term securities.) Fixed income securities also carry inflation risk, liquidity risk, call risk, and credit and default risks for both issuers and counterparties. Any fixed income security sold or redeemed prior to maturity may be subject to loss.

The S&P 500® Index is a market capitalization-weighted index of 500 common stocks chosen for market size, liquidity, and industry group representation to represent US equity performance. Indexes are unmanaged. It is not possible to invest directly in an index.

Fidelity Investments® provides investment products through Fidelity Distributors Company LLC; clearing, custody, or other brokerage services through National Financial Services LLC or Fidelity Brokerage Services LLC; and institutional advisory services through Fidelity Institutional Wealth Adviser LLC.